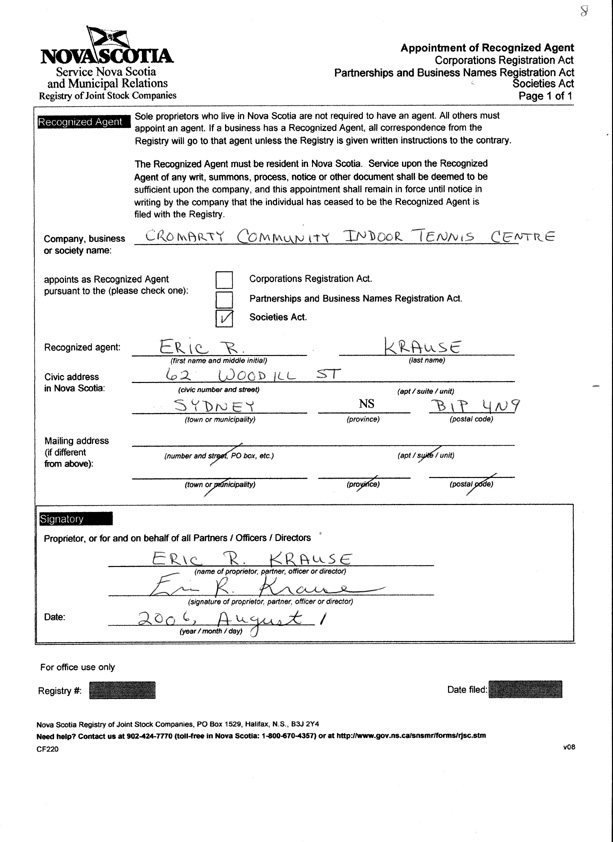

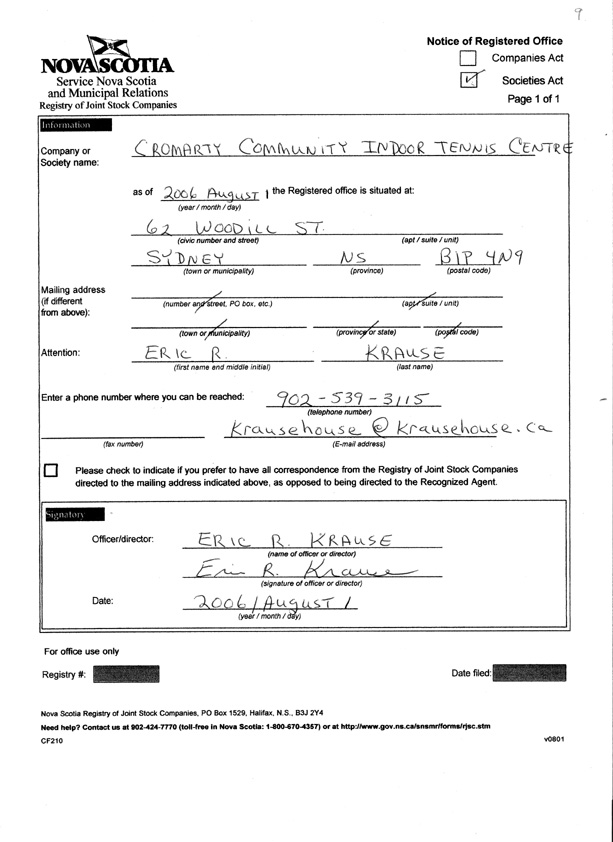

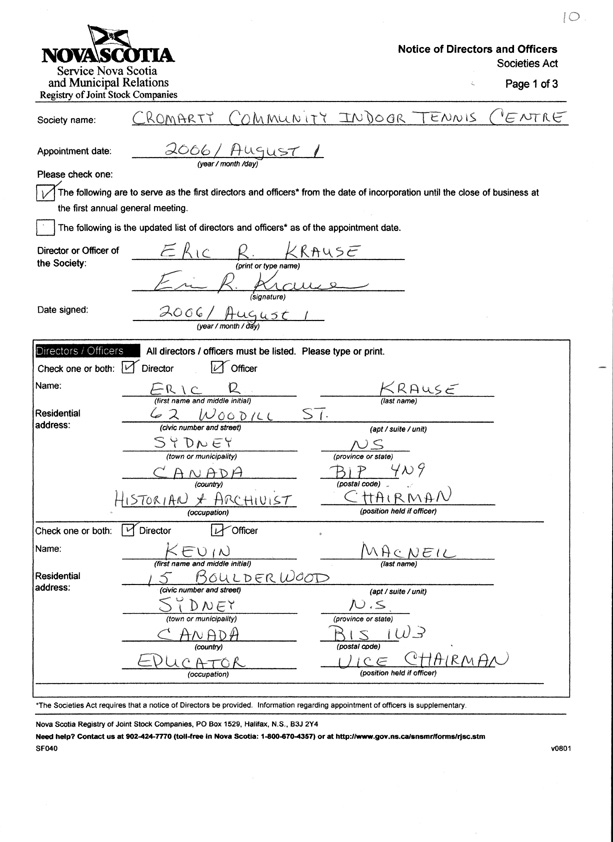

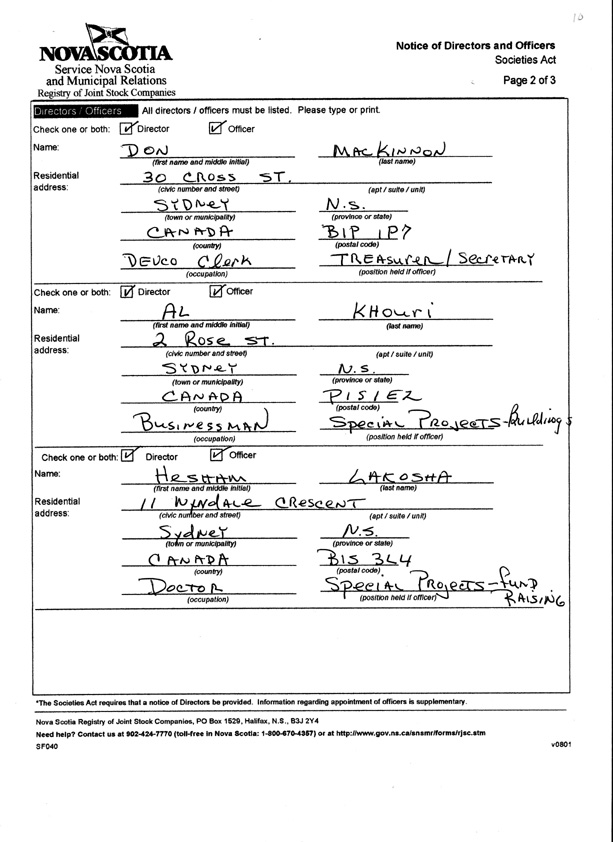

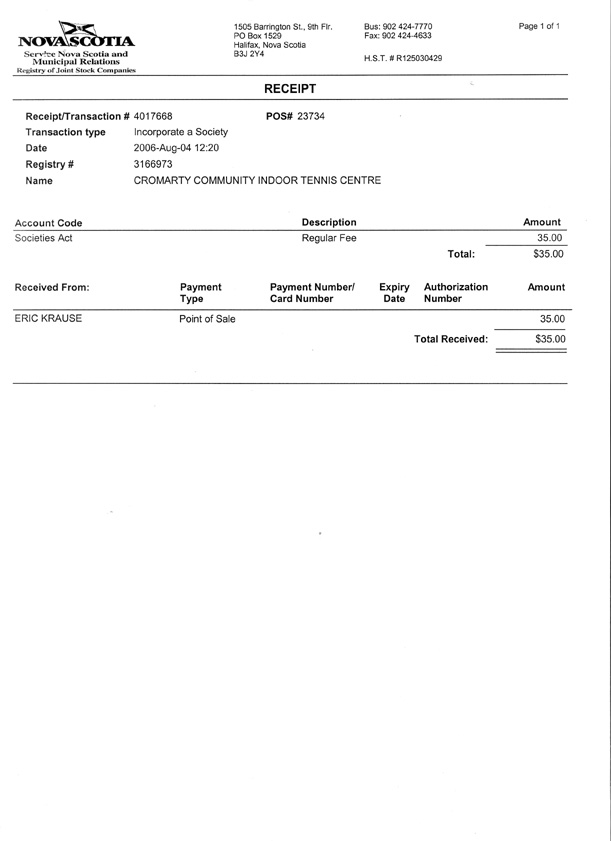

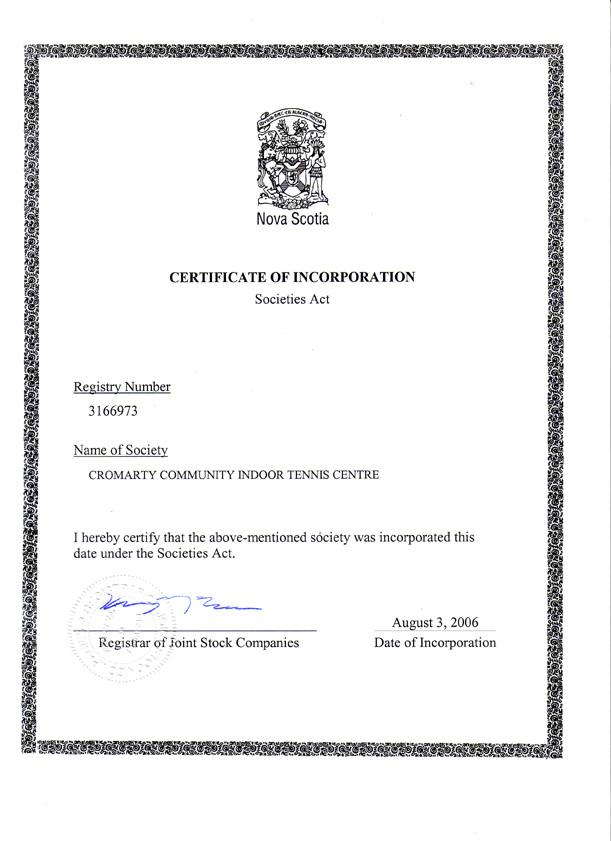

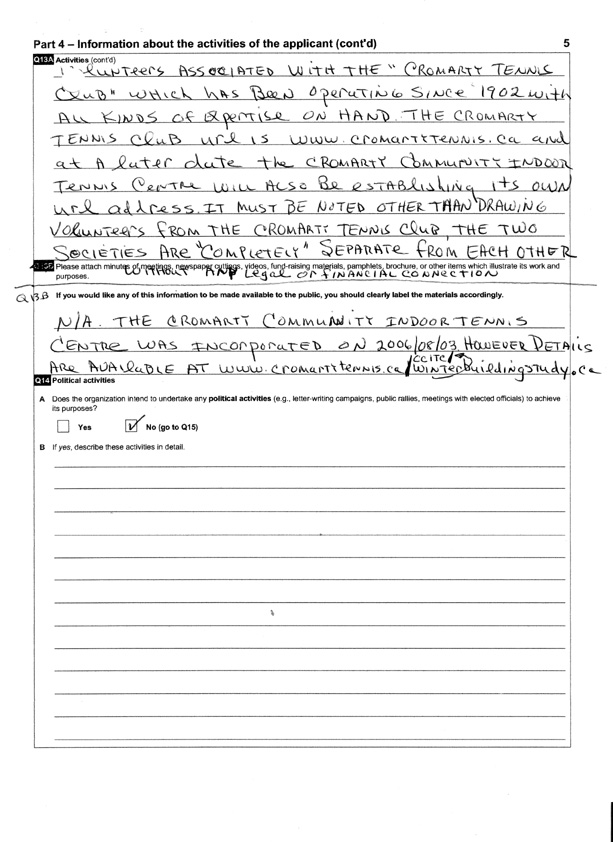

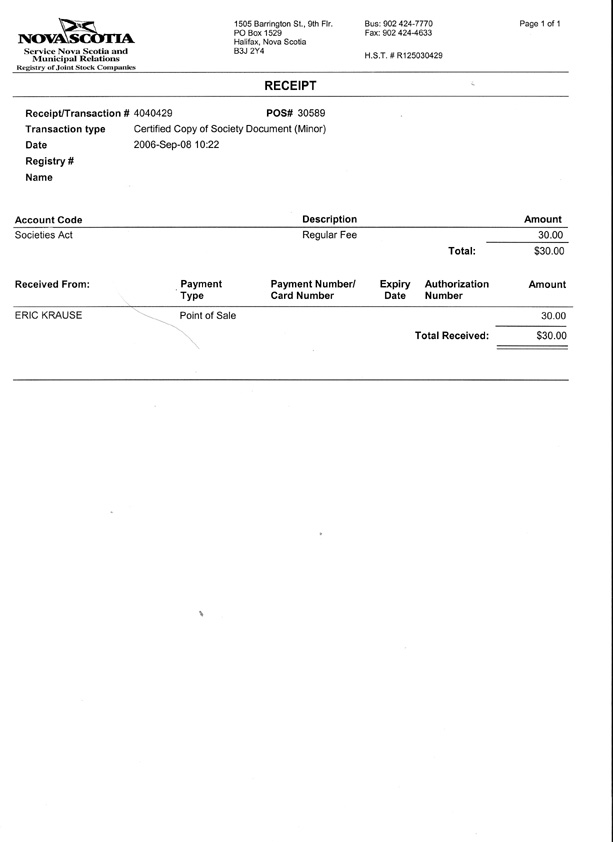

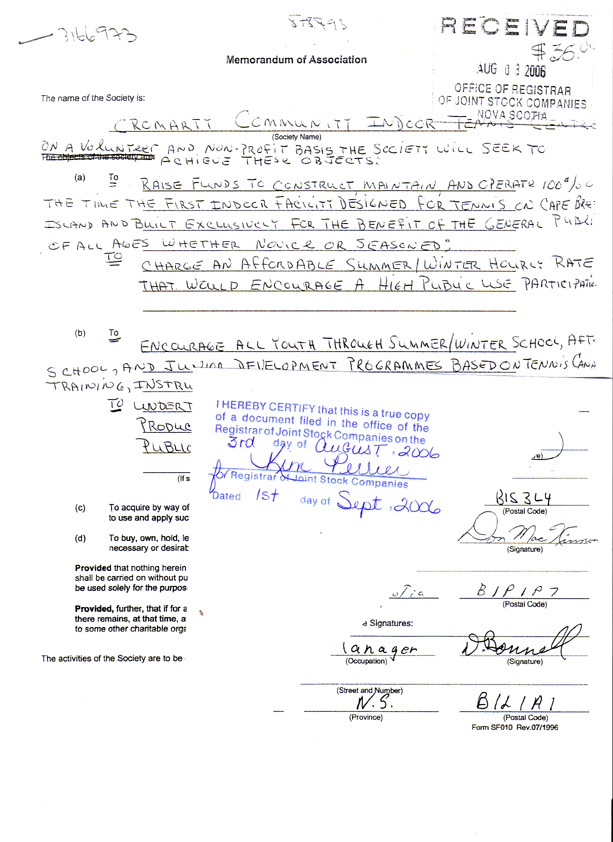

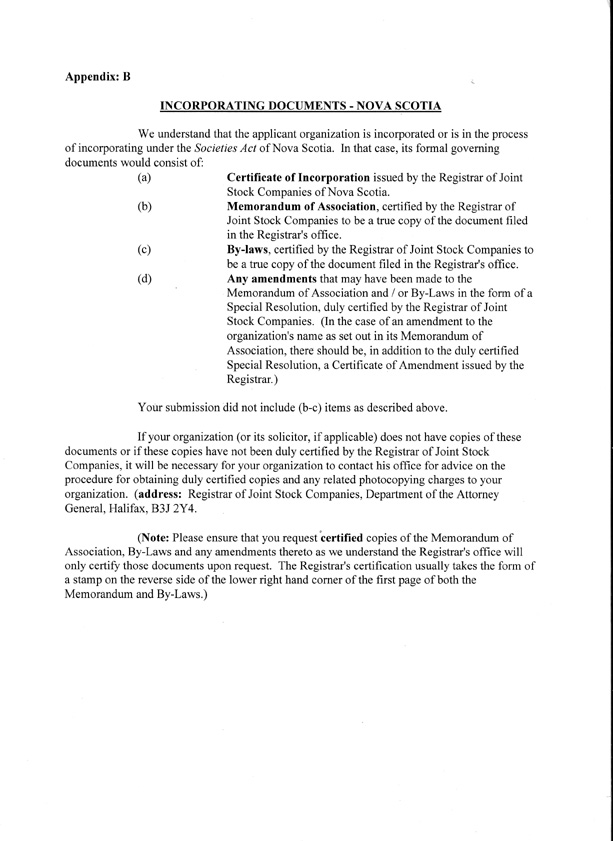

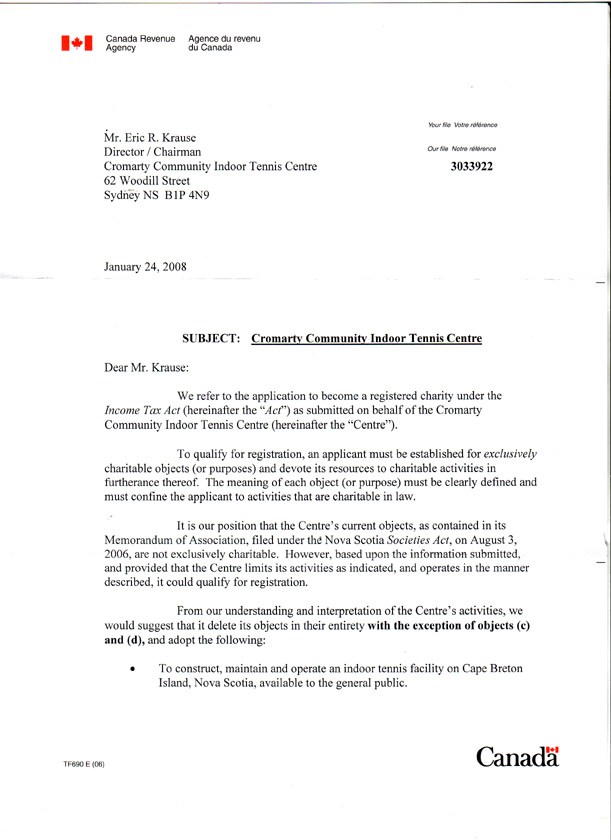

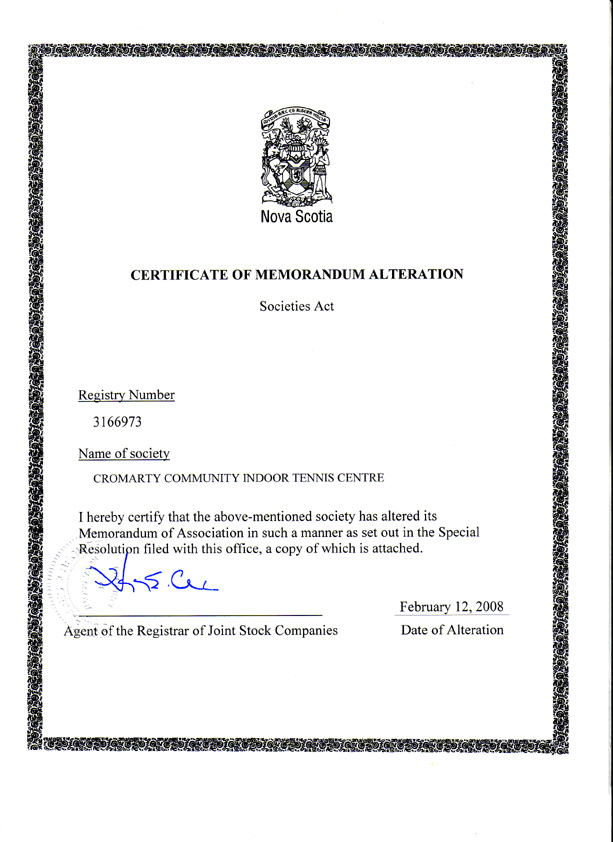

On August 3, 2006 the "Cromarty Community Indoor Centre" was incorporated as a non-profit society under the Nova Scotia Societies Act, with its registry ID being 3166973.

- ITEM 5 -

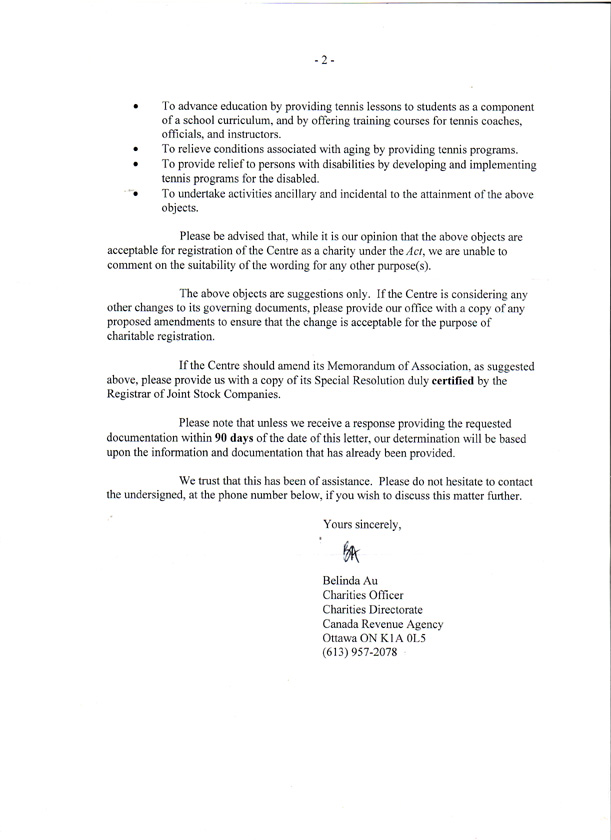

The registered Canadian charity category that the public indoor facility would meet would be number 56 (Recreation, Playgrounds and Vacation Camps). It is also critical to note that no more than 49% of the directors/trustees of the CCITC can be related persons.

The trust's mission statement:

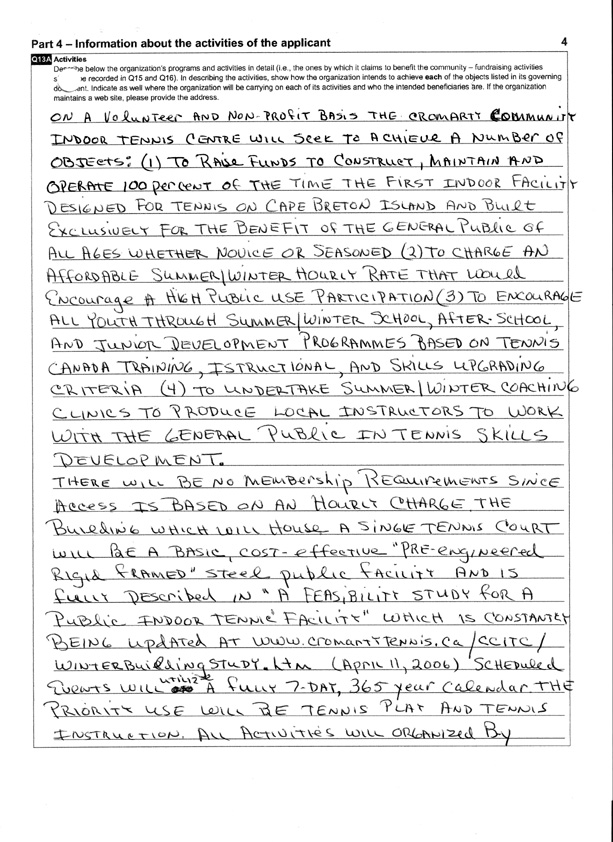

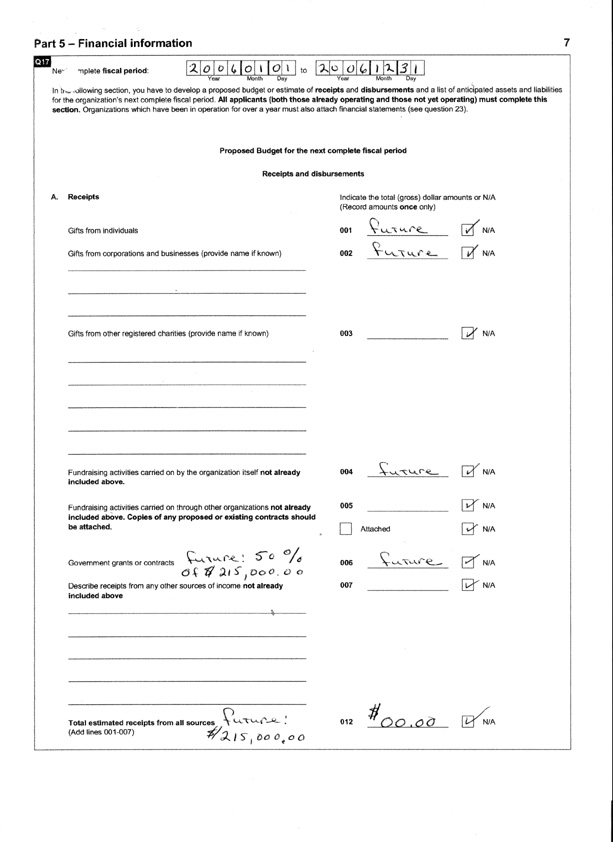

For the Cromarty Tennis Club, through an independent trust, known as the Cromarty Community Indoor Tennis Centre (CCITC), to raise funds to construct, maintain, and operate Cape Breton’s first indoor facility (one covered doubles court) designed only for tennis. An all-season operation, the Centre will feature programmes that without exception will be CCITC run and designed. Where practical, that design will meet Tennis Nova Scotia, or Tennis Canada standards.

Built exclusively for the benefit of the public, with a particular focus on the young, old, and the challenged, the Centre will provide a summer/critical winter playing venue for all levels and ages of tennis players, from novice through seasoned. It will encourage high public user participation rates through an affordable hourly rate - first come, first serve - and educational group clinics. It will stress that its cushioned court is state-of-the-art and exceptionally physically friendly, to draw in the older player who might hesitate to participate otherwise.

The Centre will stress public instruction, at both an hourly and clinic level. At the hourly level, CCITC trained staff volunteers will provide tennis advice, knowledge, practical tips, and even racquets upon the asking, at no additional charge.

In addition, the Centre will target the younger public, through assorted winter and summer group clinics. It will maximize the number of operating hours to what is practical. In particular, the Centre will concentrate on winter school, winter after school, and winter junior development programmes based on Tennis Canada training, instructional, and skills upgrading criteria. Winter coaching clinics would be another priority, as would other community group initiatives, such as wheelchair and mixed senior (plus 55) play.

During the summer, held will be similar group clinics designed to enhance any Island outdoor programme that requests CCITC help.

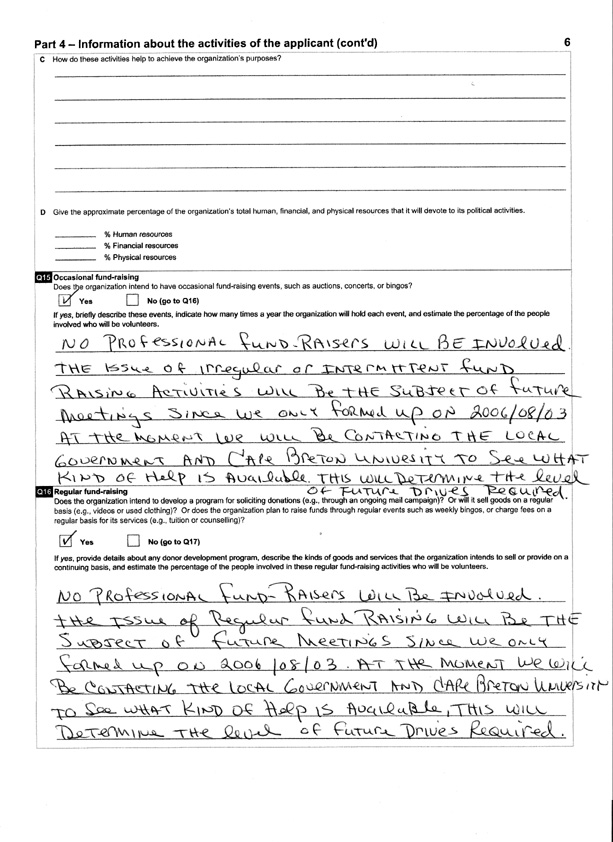

Throughout the year, winter and summer, the community Centre will interact with Cape Breton schools, the Cape Breton Regional Municipality (regional government), local community clubs (including tennis), and the public at large in growing the game, and building a healthy community. To achieve these goals, the Centre will depend upon volunteers from the local tennis community who have already shown a keen interest in helping the Centre.

The Centre will develop a range of varied programmes. Without exception, they will focus upon the public needs of the community, in particular upon the younger, senior, and challenged player of any age, or ability. Thus, they would include, but not be limited to, scheduled group tennis development, wheelchair playing, and mixed senior (55 plus) doubles play.

Although the Centre's daily operating hours would depend upon demand, each scheduled programme would receive a guaranteed number of hours, beyond which more time was always possible. The Centre would devote all possible resources to achieving their goals.

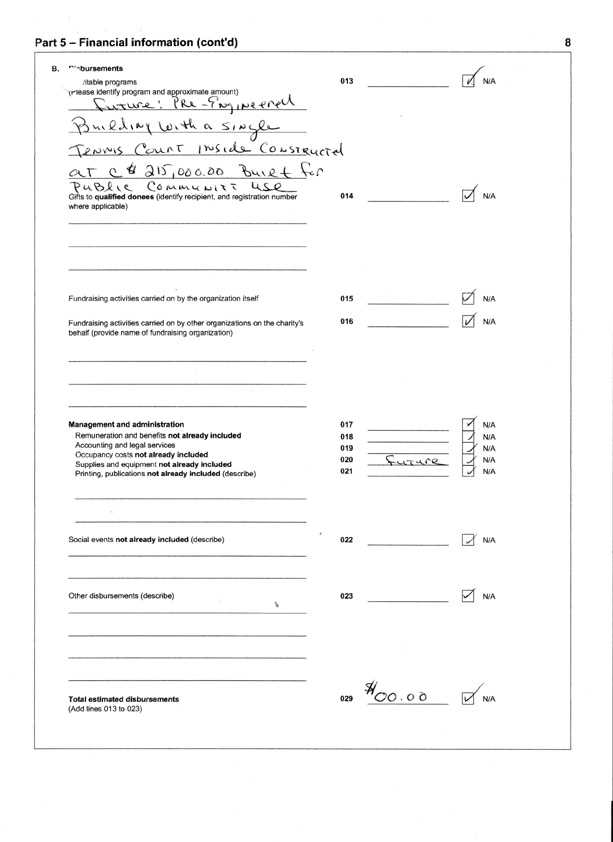

Some examples (Note - the CCITC building consists of only one doubles court):

(A) GROUP TENNIS DEVELOPMENT (Racquets always available upon request, at no charge)

(1) Winter School Clinic (5-18 years of age)

(a) Different schools with different tennis days to learn to play tennis and practice afterwards under supervision

(b) Day time sessions during school hours - Five Weekdays: 2 hours per day=10 hours per week(2) Winter After-School Clinic (5-18 years of age)

(a) Lessons based on skills progression to take an individual over time from beginner to supervised play. Includes an entry-level program for kids aged 5-11 with the transition from mini-tennis to full-court tennis

(b) Day time sessions after school - Four Weekdays (4 pm-6 pm), 2 hours per day= 8 hours per week(3) Winter Junior Development Clinic (Under 18 years of age)

(a) Under 14 Players: Designed to help develop athletes beyond supervised play to an advanced level and tournament play

(b) 15-18 Players: Those who have graduated from the "Under-14" program. A systematic development plan over time so that older aged seasoned juniors can fulfill their potential through the growth of an individual game style under Coach supervision

(c) Day time sessions after school - One Weekdays (4 pm-6 pm), 2 hours per day= 2 hours per week

(d) Weekend sessions - Two Weekend days, 2 hours per day= 4 hours per week(4) Winter Coaching Clinics

Coaching Clinics (Prepare future coaches to take their certification courses offered by Tennis Nova Scotia and Tennis Canada). The clinic will utilize local certified volunteers. These future coaches will volunteer some time to the Centre’s school programmes as well.

(a) Tennis Instructor (15 years of age and older)

(i) Provides the knowledge, communication and implementation skills to set-up and run drills for group lessons from the 1.0 to 2.5 levels

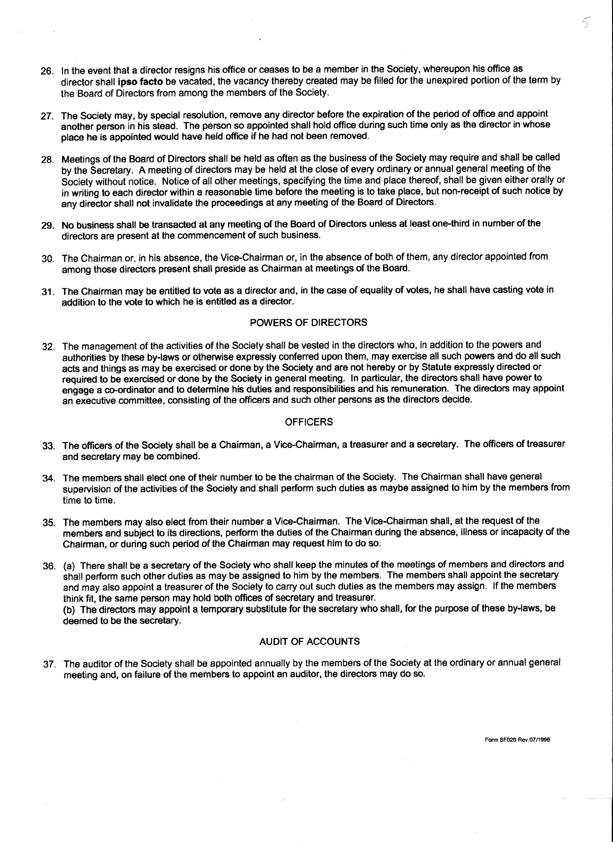

(ii) Follows the Tennis Canada Guide: Tennis Instructor Manual – Sixth Edition September 2006(b) Club Pro 1 (15 years of age and older)

(i) Allows giving lessons successfully; running teams successfully; planning a lesson program; running a tennis-specific warm-up; drill organization; feeding; giving feedback; dingles strategy and tactics; technical development; coaching wheelchair tennis players; running a job search.

(ii) Ability to implement the most common on court activities for the 1.0 - 3.5 level player

(iii) Follow the Tennis Canada Guide: Club Pro 1 Manual – 6th Edition January 2007

(iv) Follow the Tennis Canada Guide: Tennis Canada Wheelchair Tennis Instructor Certificate Course Manual - August 2003

(v) Follow the Tennis Canada Guide: Wheelchair Tennis Doubles Manual – February 2006(c) Weekend sessions - Two Weekend days, 1 hour per day= 2 hours per week

(B) WHEEL CHAIR PLAY

(1) Wheel Chair Tennis promotion through introductory clinics

(2) The Centre will provide the proper chairs and racquets upon request, no charge

(3) Demand will determine the number of hours(C) MIXED (MALE/FEMALE) SENIOR (55 plus) DOUBLES PLAY (Racquets always available upon request, at no charge)

(1) The Centre will set up the teams and schedule the play

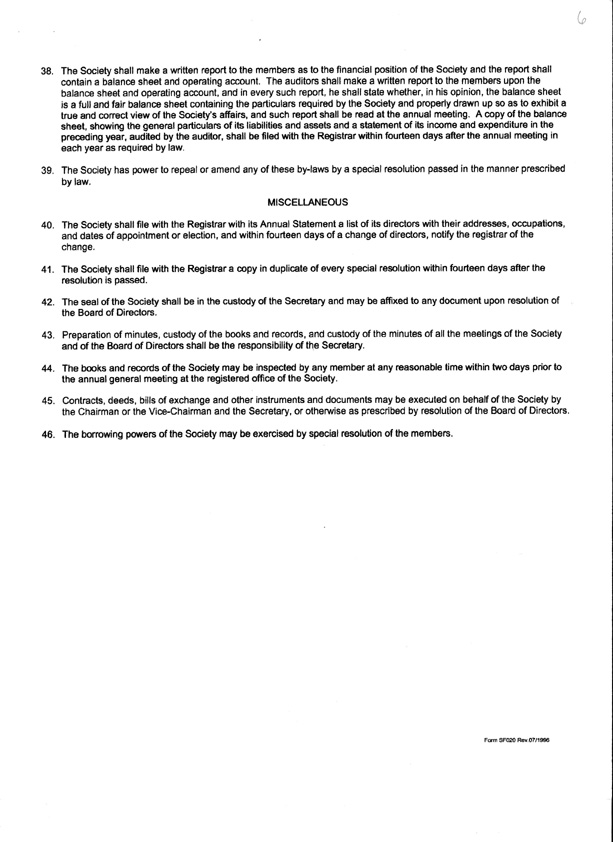

(2) Free tennis instructor available to teach basics

(3) Day time sessions - Five Weekdays: 2 hours per day=10 hours per week

- ITEM 6 -

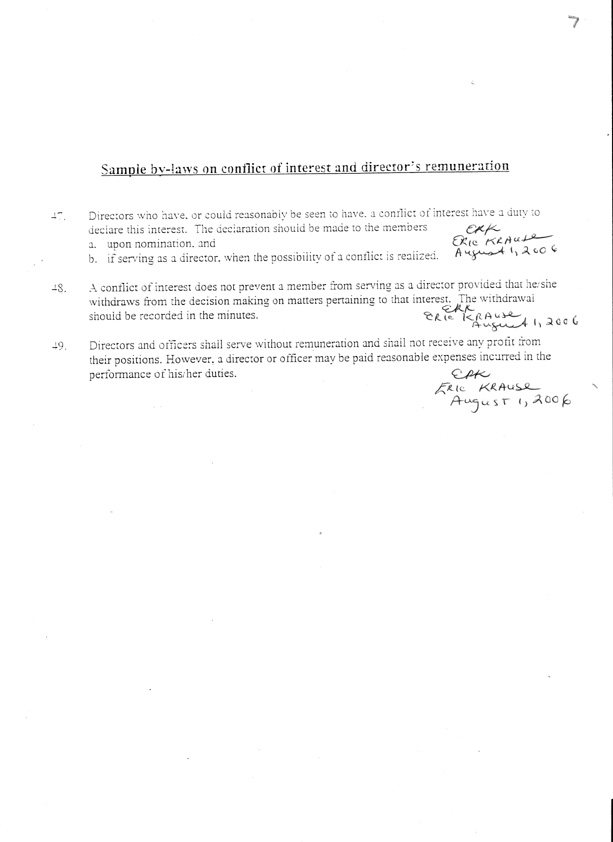

On June 6 (Amended August 1, 2006), the following application was sent to Joint Stocks: